First published in the Daily Maverick 168 weekly newspaper.

Answer: A discretionary investment plan can certainly solve a lot of your problems. I have used it to great effect for a number of my retired clients.

A discretionary investment plan is a lot like a living annuity without any of the living annuity restrictions. Because a living annuity is funded by the proceeds of a pension fund or retirement annuity (where you received tax benefits when you invested), you are not allowed to access the capital. You’re only allowed to draw down between 2.5% and 17.5%.

This is not the case with a discretionary income plan. These investments are typically funded from other savings or the sale of assets such as a property or a business.

With the income plan:

You can draw down on a monthly, quarterly or annual basis; and

You can change the income amount whenever you like; and the regular drawdown may not be more than 20% of the capital in a year. You may, however, draw out an ad hoc amount whenever you like.

How much should you draw each month?

This is a key decision. If the income you draw is too high, then you will start using up your capital and you stand a chance of running out of money.

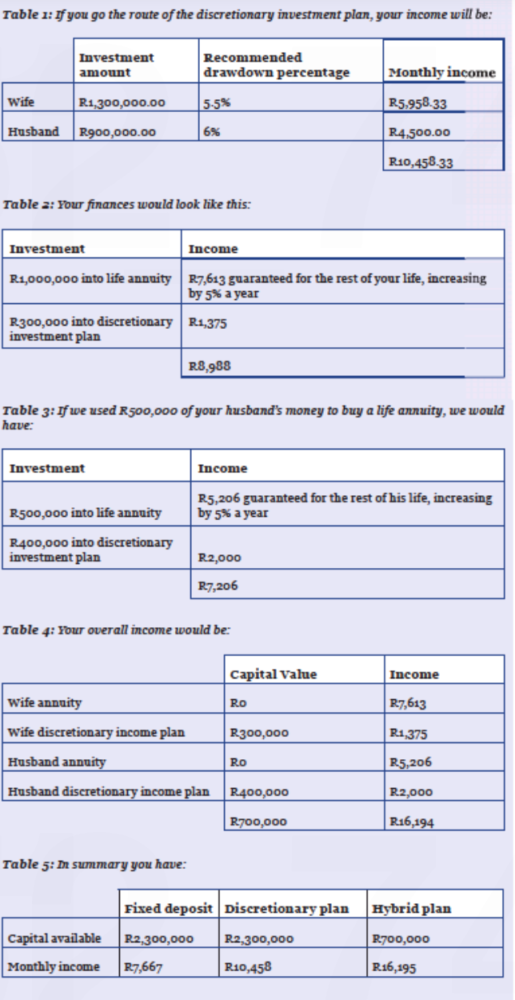

We can use the Financial Sector Conduct Authority’s guidelines on living annuities to help us select the right rate for you. As a 75-year-old, you may draw down 5.5% of your investment. If you draw more than 8%, you will run into trouble. As he is 80, your husband may draw down between 6% and 9.5% (see Table 1).

How to improve your cashflow

Life annuity rates are really good at the moment. A life annuity is like a pension. You receive an amount each month, which increases each year. When you die, it stops or pays out a spouse’s pension.

I recommend to my retired clients that they take out a life annuity to cover their basic costs such as medical, rent and food.

I ran a quote for you where we use R1-million of your savings to buy a life annuity that will increase by 5% each year for the rest of your life (see tables 2 to 4).

As you can see, this will make a massive difference to your cashflow.

You must, however, bear in mind that with the second scenario, there will only be R700,000 instead of the R2.3-million for your heirs to inherit. But you will be trading this for a much higher level of financial security. Remember the life annuity will increase by 5% each year (see Table 5).

By shopping around, you may be able to improve your fixed deposit income.

The solution I gave above is based on a very limited knowledge of your financial situation.

The products I mentioned have a number of features that could be tweaked to provide you with a better solution to your specific needs. Your financial adviser should be able to help you achieve this. DM168

This story first appeared in our weekly Daily Maverick 168 newspaper which is available for free to Pick n Pay Smart Shoppers at these Pick n Pay stores.

You say that Life Annuities are good “right now”. What are the implications of making this investment now, and in a few years, when they are not good, being able to change investment? I am a bit thick when it comes to these things, so forgive me if this is obvious.